")

We have a real problem.

In speaking with CNN’s Erin Burnett, Summers said, “the real concern is that we are going to get a wage/price spiral. That is still a substantial risk.”

Academic Research on Tax Compliance

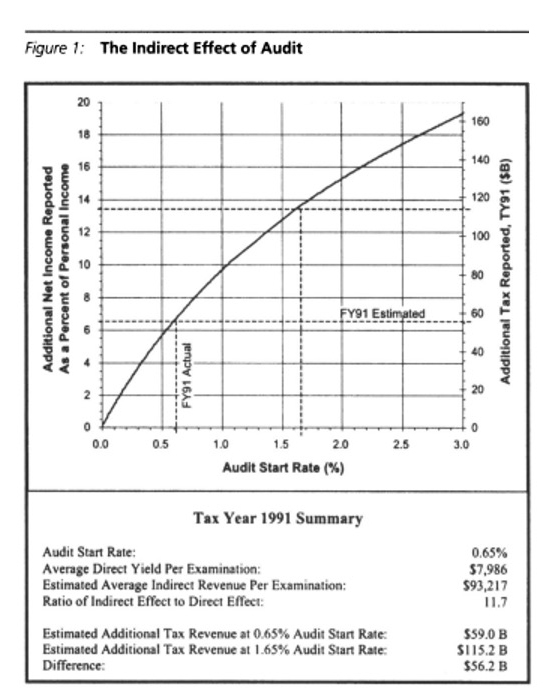

- Early 1996, IRS study compared cross-state differences in audit rates to find the average indirect effect from started audits was about 12 times as large as the direct additional taxes imposed following completed audits that year (Plumley 2002).

- Dubin (2007) relies on IRS examination data for individual filers to conclude that the spillover or indirect effects are at least nine times as large as the direct revenue effects from compliance efforts.

- Hoopes, Mescall, and Pittman (2012) study corporate tax avoidance and find that a doubling of the audit probability increases effective tax rates by 7 percent.

- Alm, Jackson, McKee (2009): Overall, our results yield an estimate of the indirect effect on compliance of 4.4 times the direct effect on compliance, an estimate that falls within the range of estimates from field data.

- Slemrod, Blumenthal, and Christian (2001): Finds although low and middle-income taxpayers substantially increase tax payments if they expect to be audited, reported tax liability for high-income filers actually falls. [direct deterrent effects, our interest is indirect/general deterrence effects]

- DeBacker, Heim, Tran, and Yuskavage (2018) finding that after audits, most individuals become more careful about tax filings, at least in the short-run, but that sophisticated individuals and corporations actually become more aggressive in their misreporting. [direct deterrent effects, our interest is indirect/general deterrence effects]

- DeBacker et al (2018) find that increased income reported in the 5-8 years following a random individual audit is about 1.5 times the revenue generated by the audit itself.

- US Treasury (2019): IRS returns on investment are likely understated because they ignore deterrence effects, which are conservatively estimated to be at least three times the direct revenue effect.

- Boning et al. (2020) find that in-person collection visits raise as much (1) revenue from firms sharing a tax preparer with the visited firm as from the visited firm itself

- Alm (2019): Audits also typically have a ‘spillover’ effect, or an increase in compliance independent of revenues generated directly from the audits themselves, whose magnitude varies from 4 to 12 (e.g., “general deterrence”).

Sources:

Plumley, Alan H. 2002. “The Impact of the IRS on Voluntary Tax Compliance: Preliminary Empirical Results.” In 95th Annual Conference on Taxation. National Tax Association.

DeBacker, Jason, Bradley T. Heim, Anh Tran, and Alexander Yuskavage. 2018. “Once Bitten, Twice Shy? The Lasting Impact of Enforcement on Tax Compliance.” The Journal of Law and Economics 61(1): 1-35.

Dubin, Jeffrey. 2007. “Criminal Investigation Enforcement Activities and Taxpayer Noncompliance.” Public Finance Review 35(4): 500-529.

Hoopes, Jeffrey L., Devan Mescall, and Jeffrey A. Pitman. 2012. “Do IRS Audits Deter Corporate Tax Avoidance?” The Accounting Review 87(5): 1603-1639.

Slemrod, Joel, Marsha Blumenthal, and Charles Christian. 2001. “Taxpayer Response to and Increased Probability of Audit: Evidence from a Controlled Experiment in Minnesota.” Journal of Public Economics 79(3): 455-483.

US Treasury. 2019. “FY 2019 Budget in Brief: Internal Revenue Service, Program Summary by Budget Activity.” US Treasury, Washington, DC.

DeBacker, J., Heim, B.T., Tran, A., & Yuskavage, A. 2018. “The Effects of IRS Audits on EITC Claimants.” National Tax Journal 71(3): 451-484.

Boning, W.C., Guyton, J., Hodge, R., & Slemrod, J. 2020. “Heard it through the grapevine: The direct and network effects of a tax enforcement field experiment on firms.” Journal of Public Economics 190(3-4): 104261.

Alm, James, Betty R. Jackson, and Michael McKee. “Getting the word out: Enforcement information dissemination and compliance behavior.” Journal of Public Economics 93.3-4 (2009): 392-402.

Alm, James. “What motivates tax compliance?.” Journal of Economic Surveys 33.2 (2019): 353-388.

CNN’s Cuomo Prime Time

I don’t think Build Back Better is an inflation problem. I think a lot of it is vitally needed investments in the future of our country.

CNN’s New Day on Debt Ceiling Risks

Talked with Brianna Keilar of CNN New Day on the debt ceiling risks saying, “The credit of the United States going back to Alexander Hamilton is a fundamental national asset.”

Former Treasury Secretary On Consumer Prices, Inflation, U.S. Role In Global Pandemic Efforts

Here & Now’s Scott Tong speaks with Larry Summers, who was Treasury Secretary under former President Bill Clinton, director of the National Economic Council under former President Barack Obama. He’s now president emeritus of Harvard University.

Summers discusses the risks of inflation and how government spending on infrastructure will strengthen the economy.

Shrinking the Tax Gap: A Comprehensive Approach

In Tax Notes, former IRS Commissioner Charles Rossotti, Natasha Sarin and and I outline how the Biden Adminstration can collect more than $1 trillion in a highly progressive way: Making people pay the taxes that they already owe.

Fiscal policy advice for Joe Biden and Congress

At an event sponsored by Brookings and PIEE, Jason Furman and I presented a paper, A Reconsideration of Fiscal Policy in the Era of Low Interest Rates, arguing that persistently low interest rates require a rethinking of the framework for fiscal policy.

Tackling the Tax Code

The Hamilton Project

Brookings Institute, Washington, DC

January 28, 2020

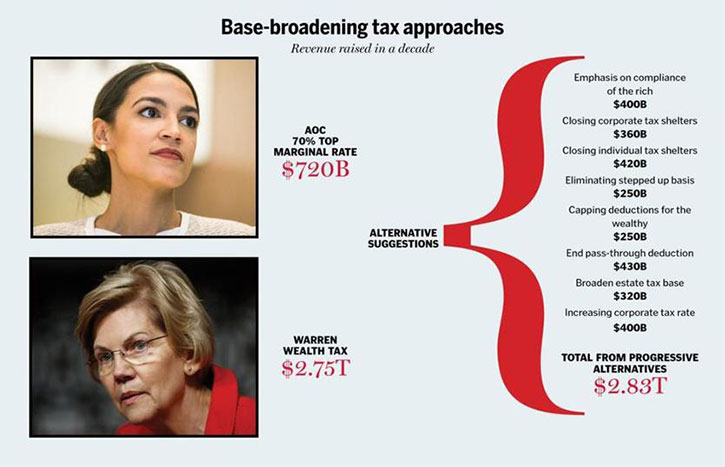

A broader tax base that closes loopholes would raise more money than plans by Ocasio-Cortez and Warren

By Natasha Sarin and Lawrence H. Summers

March 28, 2019

First of two parts

Tax reform debates have been transformed in recent weeks by a shift in emphasis from revenue raising and progressivity to an emphasis on going after the rich for the sake of equality and justice. Bold proposals from Representative Alexandria Ocasio-Cortez of New York, for a 70 percent marginal tax rate on top earners, and from Senator Elizabeth Warren of Massachusetts — a 2020 Democratic presidential candidate — for a wealth tax on those worth more than $50 million have attracted widespread attention.

Warren’s proposal aspires to raise roughly 1 percent of GDP ($2.75 trillion in the next decade). Ocasio-Cortez’s proposal is estimated to generate around one-third of 1 percent ($720 billion in the next decade). By way of comparison, the Trump tax cuts will cost the federal government about $2 trillion over the next decade. We agree with Ocasio-Cortez and Warren that increases in tax revenue of at least this magnitude are necessary. We also agree that the way forward is by generating more revenue from the most affluent Americans. Indeed, it may well be necessary and appropriate to raise more than Warren’s targeted 1 percent of GDP from those at the top.

Where we differ from Warren and Ocasio-Cortez is in our belief that the best way to begin raising additional revenue from highest income tax payers is with a traditional tax reform approach of base broadening and loophole closing, improved compliance, and closing of shelters. We show that these measures, along with partial repeal of the Trump tax cut, can raise far more than recent proposals. These measures will increase economic efficiency, make our tax system more fair, and are perhaps more politically feasible than a wealth tax or large hikes of top rates. It may be that measures beyond base-broadening are appropriate and desirable given the magnitude of the revenue challenge we face. But base-broadening is the right place to begin.

Below we outline proposals for broadening the tax base that meet a stringent test: These are measures that would be desirable even if we did not have revenue needs. They are progressive and attack those who have received special breaks for too long. And together, the revenue-raising potential of these measures exceeds that of the 70 percent top rate or the wealth tax. We believe this is where the progressive tax policy debate should begin.

Emphasis on compliance and auditing of the rich. In 2017, the IRS had only 9,510 auditors — down from over 14,000 in 2010. The last time the IRS had fewer than 10,000 auditors was in the mid-1950s. Since 2010, the IRS budget has decreased by over 20 percent in real terms. The result is that individuals and corporations are shirking their responsibilities: The most recent estimate by the IRS suggests that taxpayers paid only around 82 percent of owed taxes, losing the IRS over $400 billion a year.

The Congressional Budget Office estimates that spending an additional $20 billion on enforcement in the next decade could bring in $55 billion in additional tax revenues. This excludes the indirect deterrent effects of greater enforcement, which the Treasury Department has estimated are three times higher. Outlays at this level would still leave the IRS operating with budgets in real terms that were nearly 10 percent below peak levels, which themselves were leaving large amounts of revenue on the table.

In addition to the level of investment in enforcement, there is the question of the allocation of enforcement resources. It has been estimated that an extra hour spent auditing someone who earns more than $1 million a year generates an extra $1,000 in revenue. And yet in 2017 the IRS audited only 4.4 percent of returns with income of $1 million or higher, less than half the audit rate a decade prior. Remarkably, recipients of the earned income tax credit, who never have incomes above $50,000, are twice as likely to be audited as those who make $500,000 annually.

No one can know exactly the potential for increased enforcement to raise revenue. Suppose instead of investing an extra $20 billion over the next decade, we invested $40 billion and focused on wealthy taxpayers, perhaps taking the audit rate for million-dollar earners up to 25 percent. Considering the direct benefits and the multiplier from deterrence, it is not unreasonable to suppose that over a decade $300 billion to $400 billion could be raised.

This revenue increase — unlike a revenue increase from new taxes or higher rates — will have favorable incentive effects. It will encourage people to participate in the above-ground economy. And what could be more of a step toward fairness than collecting from wealthy scofflaws?

Closing corporate tax shelters. All too often, corporations are able to make use of tax havens, differences in accounting treatment across jurisdictions, and other devices to reduce tax liabilities. Economist Kimberly Clausing estimates that profit-shifting to tax havens costs the United States more than $100 billion a year. Although the Trump tax plan sought to reduce the incentives for profit-shifting, various exemptions and design flaws mean that the new system does little to deter shifting revenues to tax havens. Fairly incremental changes will have a large impact: For example, a per-country corporate minimum tax rather than a global minimum tax will increase tax revenues by nearly $170 billion in a decade.

But there is much more to be done. A robust attack on tax shelters — that included, for example, tariffs or penalties on tax havens as well as stricter penalties for lawyers and accountants who sign off on dubious shelters — could raise twice the revenue attainable from a per-country minimum tax, or about 30 billion annually. It would also encourage the location of economic activity in the United States and discourage the vast intellectual ingenuity that currently goes into tax avoidance.

Closing individual tax shelters. Like the corporations they own, wealthy individuals make use of myriad loopholes in the tax code to shelter their personal income from taxation. Most high-income taxpayers pay a 3.8 percent tax that pays into entitlement programs like Social Security and Medicare. However, some avoid these payroll taxes by setting up pass-through businesses and re-characterizing large shares of their income as profits from business ownership, rather than wage income. The Obama administration’s proposals to close payroll tax loopholes were estimated to generate $300 billion over a decade.

Another egregious loophole is 1031 exchanges, which allow real estate investors to sell property, take a profit, and defer paying taxes on those profits so long as they reinvest them in similar investments. There is no limit on the number of these exchanges that investors can make. Consequently, the wealthy use 1031 exchanges to build up long-term tax-deferred wealth that can eventually be passed down to their heirs without taxes ever being paid. Outright repeal of 1031 exchanges were estimated in 2014 to raise around $40 billion in a decade and would raise almost $50 billion today.

Another tool used to shelter individual income from taxation is carried interest. Income that flows to partners of investment funds is often treated as capital gains and taxed at lower rates than ordinary income. This creates a tax-planning opportunity for investors to convert ordinary income into long-term capital gains that receive much more generous tax treatment. President Trump repeatedly vowed that his signature tax cuts would eliminate the carried-interest loophole, saying it was unfair that the ultra-wealthy were “getting away with murder.” However, in the face of significant lobbying pressure, the administration abandoned these plans. The Joint Committee on Taxation estimates that taxing carried profits as ordinary income would generate over $20 billion in a decade.

Other ways in which individuals can shelter income include misvaluing interests such as shares in investment partnerships when putting them in retirement accounts as well as schemes involving nonrecourse lending.

Closing tax shelters would level the playing field in favor of investments by companies that create jobs and to the detriment of various kinds of financial operators. This would raise employment and incomes as well as contributing to fairness.

Eliminating “stepped-up basis.” Wealth tax advocates rightly point to an important gap in our current system. An entrepreneur starts a company that turns out to be highly successful. She pays herself only a small salary, and shares in the company do not pay dividends, so the company can invest in growth. The entrepreneur becomes very wealthy without ever having paid appreciable tax, as the income that made the wealth possible represents unrealized capital gains.

Unrealized capital gains explain how Warren Buffett can pay only a few million dollars in taxes in a year when his wealth goes up by billions. Astoundingly, no capital gains tax is ever collected on appreciation of capital assets if they are passed on to heirs. Specifically: When an investor buys a stock, the cost of that purchase is the tax basis. If the stock rises in value and is then sold, the investor pays taxes on the gains. If an investor dies and leaves stock to her heir, that cost basis is “stepped up” to its price at the time the stock is inherited. The gain in value during the investor’s life is never taxed.

Implementing the Obama administration’s proposals for constructive realization of capital gains at death would raise $250 billion in the next decade. This is a progressive change that would impact only the very wealthy: Ninety-nine percent of the revenue from ending stepped-up basis will be collected from the top 1 percent of filers.

Eliminating stepped-up basis will also make the economy function better and so would be desirable even if it did not raise revenue. The fact that capital gains passed on to children entirely escape taxation provides aging small-business owners or real estate owners a strong incentive not to sell them to those who could operate them better while they are alive. It also makes it much more expensive to realize capital gains and use the proceeds to make new investments than it would be if the capital gains tax was inescapable.

Capping tax deductions for the wealthy. Today, a homeowner in the top tax bracket (post-Trump tax cuts, 37 percent) who makes a $1,000 mortgage payment saves $370 on her tax bill. Under an Obama administration proposal to limit the value of itemized deductions to 28 percent for all earners, that same write-off would save this wealthy taxpayer just $280. Importantly, such a cap would raise tax burdens only for the rich: Those with marginal rates under the cap would still be able to claim the full value of their itemized deductions. The plan to cap top-earners’ itemized deductions was estimated to raise nearly $650 billion in a decade. Recognizing that the Trump tax plan scaled back the mortgage interest deduction and state and local tax deductions, we estimate that additional limits on top-earner deductions could generate around $250 billion in a decade.

As with the elimination of stepped-up basis, the distributional case for capping tax deductions is strong. The mortgage interest deduction provides a tax advantage to homeowners; promoting homeownership is a worthy goal. But there is little rationale for subsidizing home ownership at higher rates for richer rather than poorer taxpayers.

End the 20 percent pass-through deduction. Perhaps the most notorious of the Trump tax changes, the pass-through deduction provides a 20 percent deduction for certain qualified business income. This exacerbated the tax code’s existing bias in favor of noncorporate business income and so reduces economic efficiency. And the complex maze of eligibility is arbitrary, foolish, and a drain on government resources: The Joint Committee on Taxation estimates that this provision will reduce federal revenues by $430 billion in the next decade. Eliminating the pass-through deduction will reduce incentives for tax gaming and raise revenue primarily from taxpayers making more than $1 million annually.

Broaden the estate tax base. Prior to the Trump tax reform, only 5,000 Americans were liable for estate taxes. The recent changes more than halved that small share by doubling the estate tax exemption to $22.4 million per couple. The Joint Committee on Taxation estimates that this change costs around $85 billion, with the benefits accruing entirely to 3,200 of the wealthiest American households. Repealing the Trump administration’s changes and applying estate taxes even more broadly — for example, as the Obama administration proposed, by lowering the threshold to $7 million for couples — would raise around $320 billion in a decade. The estate tax would still only impact 0.3 percent of decedents.

In addition to the question of the appropriate floor on estates, there is also ample room to attack the many loopholes that enable wealthy families to largely avoid paying taxes when transferring wealth to their progeny during their lifetimes. This happens through a mix of trust arrangements, intra-family loans, and dubious valuation practices to evade gift-tax liability. Strengthening the taxation of estates would raise revenue and be efficient, diverting resources from tax planning and increasing work incentives for the children of the wealthy. We are enthusiastic about proposals, notably by Lily Batchelder, that call for the conversion of the estate tax into an inheritance tax, to appropriately tax inherited privilege and discourage large concentrations of wealth.

Increasing the corporate tax rate to 25 percent. When corporations began lobbying efforts on corporate tax reform, their stated objective was a 25 percent corporate rate. Business leaders produced estimates showing how this 25 percent rate would have prevented foreign purchases of thousands of companies and shifted billions in corporate taxable income to the United States. The Trump tax cuts delivered more than the business community asked, slashing the corporate rate to 21 percent. The CBO estimates that a 1 percentage point increase in the corporate tax rate will generate $100 billion in the next decade. Based on this estimate, a 4 percentage point increase to 25 percent will generate an additional $400 billion in revenue.

Raising the corporate tax rate would not increase the tax burden on most new investment, because it would raise in equal measure the value of the depreciation deductions that corporations could take when they undertook investments. The principle losers from an increase in the rate would be those earning economic rents in the form of monopoly profits and those who had received enormous windfalls from the Trump tax cut.

Closing tax shelters used by the wealthy alone raises more revenue than Ocasio-Cortez’s proposal. And together, the reforms we propose raise far more than a 70 percent top tax rate, and more too than Warren claims her wealth tax will generate. These base-broadening, efficiency-enhancing reforms are the best way to start raising revenue as progressively and efficiently as possible. To be sure, it may well be that wealth taxation or large increases in top rates are necessary to adequately fund government activities. But we advocate these approaches only after the revenue-raising potential of base-broadening is exhausted.

Tomorrow: The challenges in the rate hike and wealth tax proposals.

2016 Homer Jones Memorial Lecture, “Secular Stagnation and Monetary Policy”

St. Louis Fed President James Bullard welcomed attendees to the annual lecture and introduced this year’s speaker, Lawrence H. Summers, one of the country’s most influential economists and policymakers.

Dr. Summers has helped steer the United States through national and international financial crises over the past two decades. He did so while serving as director of the National Economic Council (Obama administration), as secretary of the U.S. Department of the Treasury (Clinton administration) and as chief economist at the World Bank.

Summers is president emeritus and a distinguished professor at Harvard University, and he directs the university’s Mossavar-Rahmani Center for Business and Government.

The St. Louis Fed’s annual Homer Jones Memorial Lecture honors those who exemplify the highest qualities of leadership in economics and public policy. Jones (1906-1986) was a longtime research director at the St. Louis Fed, playing a major role in developing the St. Louis Fed as a leader in monetary research and statistics.

Put American foreign policy back on the pitch

July 6, 2014

A failure to engage with global economic issues is a failure to mount a strong defense

By Lawrence H. Summers

Sports coaches know that there is nothing more dangerous for a team than retreating into passivity for fear of making a mistake. Whether it is due to a desire to sit on a lead, or because of nerves following a setback, failing to advance aggressively is almost always a strategic error.

What is true in athletic competition is all too true in the life of nations. While imprudence is always unwise, excessive caution in the name of prudence or expediency can have grave consequences. A nation will never have more power or influence than it has ambition to shape the global system. A sense of fatalism can become a self-fulfilling prophecy as adversaries are emboldened and allies move either to appease adversaries or to provide for their own security.

At a time of high tension in Europe with Russian adventurism in Ukraine, pervasive conflict and instability in the Middle East, and rising tensions within Asia as China makes its presence ever more strongly and widely felt, the choices the US makes will have far reaching consequences. It is no exaggeration to say that there is more doubt about our willingness to stand behind our allies, resist aggression and support a stable global system than at any time in decades.

Effective engagement at flash points is essential but crisis response is never as good as crisis prevention. Somewhat lost as the world focuses on global hotspots is the danger that the US will abdicate from the responsibility it has undertaken for 70 years since the second world war for supporting a more integrated, increasingly rule based and faster growing global economy. It is the success of this project that explains why history played out so differently after the second world war than after the first, and it is this project that won the cold war by demonstrating that capitalism rather than communism was the best way forward for the world’s people.

At a time when authoritarian mercantilism has emerged as the principal alternative to democratic capitalism, the US Congress is flirting with eliminating the Export Import Bank that, at no cost to the government, enables US exporters to compete on a more level playing field with those of competitor nations, all of whom have similar vehicles. Only by maintaining a capacity to counter foreign subsidies can we hope to maintain a level global trading system and to avoid ceding ground to mercantilists. Eliminating the Export Import Bank without extracting any concessions from foreign governments would be the economic equivalent of unilateral disarmament.

No one with any sophistication supposes that the world has seen the last big financial crisis or that we can prosper in a world in crisis. Yet the US, having pushed successfully for big increases in IMF resources and for important reforms in its governance, is now the lone nation blocking these measures from going into effect as Congress is unwilling to pass the relevant authorizing legislation. The IMF enables us to do in the economic area what we are unable to do in the security area: place most of the burden for supporting a functioning global system on all global stakeholders.

The vital strategic thrust proclaimed in US foreign policy over the past five years has been the pivot or rebalance towards Asia. This is entirely appropriate given the shift in the global economic centre of gravity. The reality though is that little has changed. The most important potential beneficial change in the next several years would be the achievement of the Trans-Pacific Partnership. Yet the combined prospect that a deal will be negotiated and that it will receive Congressional approval seems much too low for comfort and there is little evidence that the issue commands urgency beyond the relatively narrow international trade community. The prospects for a trade agreement with Europe seem even more remote.

Then there is the economic assistance dimension. When Latin America faced a profound debt crisis in the 1980s, when the Berlin Wall fell and the nations of central Europe and the former Soviet Union needed to transform their economies, when financial crisis struck Asia in 1997, when debt burdens stunted Africa’s growth around the turn of the century, the US working with its allies and the international financial institutions crafted strong if imperfect responses to restore growth and hope. No comparably large and generous effort is visible today with respect to the Middle East or Ukraine, even as China is emerging as a larger presence in much of Africa and Latin America than the US.

A failure to engage effectively with global economic issues is a failure to mount a strong forward defense of American interests. The fact that we cannot do everything must not become a reason not to do anything. While elections may turn on domestic preoccupations, history’s judgment will turn on what the US does internationally. Passivity’s moment has passed.

The writer is Charles W Eliot university professor at Harvard and a former US Treasury secretary

The Inequality Puzzle: Piketty Book Review

Summers reviews Thomas Piketty’s book in the Spring 2014 issue of Democracy – A Journal of Ideas. Summers writes, “Once in a great while, a heavy academic tome dominates for a time the policy debate and, despite bristling with footnotes, shows up on the best-seller list. Thomas Piketty’s Capital in the Twenty-First Century is such a volume. Piketty’s treatment of inequality is perfectly matched to its moment.” Read more

Tribute to the late Gary Becker

In a TIME Magazine tribute to the late Gary Becker Summers wrote, “Gary Becker transformed his field as few scholars ever do. There are many who advance understanding in their chosen field or propose significant new theories or do important empirical testing. There are almost none who redefine the subject matter.” Read more

Questioning Impact of Austerity in UK Economy

Summers talked with BBC Radio 4 on May 9, 2014 about Britain’s recent economic performance, austerity policies and the dangers of secular stagnation. LISTEN HERE

The Future Is Not What It Used To Be

Summers discussed secular stagnation, income inequality and how technology is changing the nature of work in an interview with Martin Wolf for the BBC Radio’s program, “The Future Is Not What It Used To Be” on May 6, 2014. LISTEN HERE