Many business people think it is wonderful that we now have an Administration filled with people from business backgrounds. To a point, I relate. People who have worked primarily in the private sector bring an awareness that others sometimes lack of maintaining business confidence, which as I have often said is the cheapest form of stimulus. And for some government tasks, management experience is much more important than policy experience. That is why Bob Rubin and I worked to install a (Republican) business leader as commissioner of the IRS given its vast IT problems.

Unfortunately, just as being able in government does not equip you to step in and run a company—at least not without much help—so also business experience does not equip you to run on your own public policy and political processes.

The concerns of those who worry about business dominated government have been demonstrated all too clearly by the Trump administration’s roll-out of plans to scale back financial regulation. There are surely areas where regulation is too burdensome, particularly involving bureaucratization and small banks. But much of what was said by the President and his advisors sounds more like grousing at an East Hampton cocktail party than a serious basis for public policy reform.

The President suggested that it was a problem that many of his good friends could not get as much credit as they wanted. We do not travel in the same social circles, so I am not sure who he means. But if he is saying that real estate developers cannot get all the credit they want, that would seem a good thing. Indeed, I would submit that the financial history of the last 40 years demonstrates that often when real estate operators are thrilled about credit availability, financial crisis is only a few years away.

Gary Cohn, the former number two at Goldman Sachs now heading the NEC, asserts that “ we are not going to burden the banks with literally hundreds of billions of dollars of regulatory costs every year”. I would challenge him to document that such costs exist today, which feels to me like an “alternative fact”. Note that total bank profits last year were about 170 billion so the claim is that without excessive regulation profits would more than double.

There is room for reasonable argument about the fiduciary rule requiring that financial advisors act in the best interest of their clients. I think the case made in the Obama CEA report is very strong but I can see counter arguments. Cohn’s analogy that “this is like putting only healthy food on the menu, because unhealthy food tastes good but you still shouldn’t eat it because you might die younger” is bizarre. We do after all require food labeling, inspect food processing, and no one is suggesting that financial products be banned, only that the economic interests of advisors be disclosed.

It does not get better. Leaving aside Cohn’s statement that “we have all submitted living wills” referring to Goldman Sachs, which was a slip for a policy official, I wonder why an Administration that professes to hate “too-big-to-fail” wants to scale living wills for banks and plans for resolution way back.

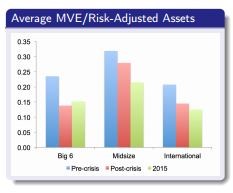

And Cohn’s argument that since banks are so well capitalized now we do not have to worry much about other aspects needs to reckon with the experience of 2008. Some of the institutions that failed, like Bear Stearns and Lehman Brothers, had capital cushions well above what both the Federal Reserve and Basel required to be labeled as “well-capitalized” in the week before their failures. Others like Goldman would likely have failed but for the bailout of their counterparties. Evidence on ratios of the market value of equity to assets suggests that even after the recent run-up, banks are operating with historically high levels of operating leverage.

I would rather live with even a very bad knee than let a carpenter operate on me. On the evidence of statements so far by those in the executive branch, the safest posture is to resist changes in the financial regulatory framework until there is proof that they have been thought through carefully. If and when this happens, there will be room to promote the flow of credit, reduce bureaucratic burdens, and make the financial system safer.