As I argued in the first blog in this series last week, I was disappointed in what came out of Jackson Hole for three reasons. The first reason, developed in that blog, was that the Fed should have signaled a desire to exceed its two percent inflation target during periods of protracted recovery and low unemployment and in this context to signal that a rate increase was off the table for September and quite likely the rest of the year. Friday’s employment report further strengthens the case for delay both by adding to the evidence on the absence of inflation pressures and by suggesting a less robust economy than most expected.

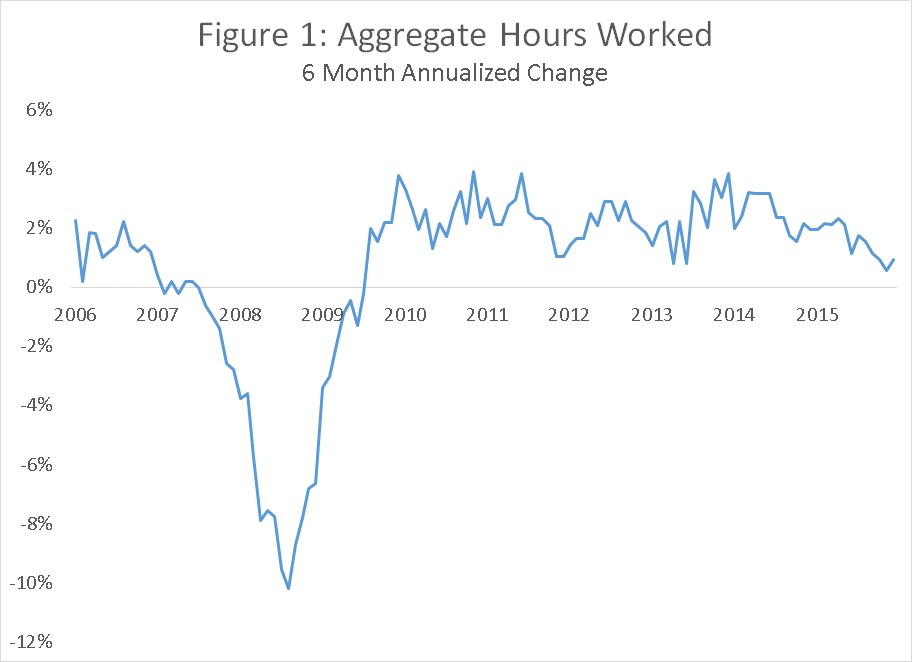

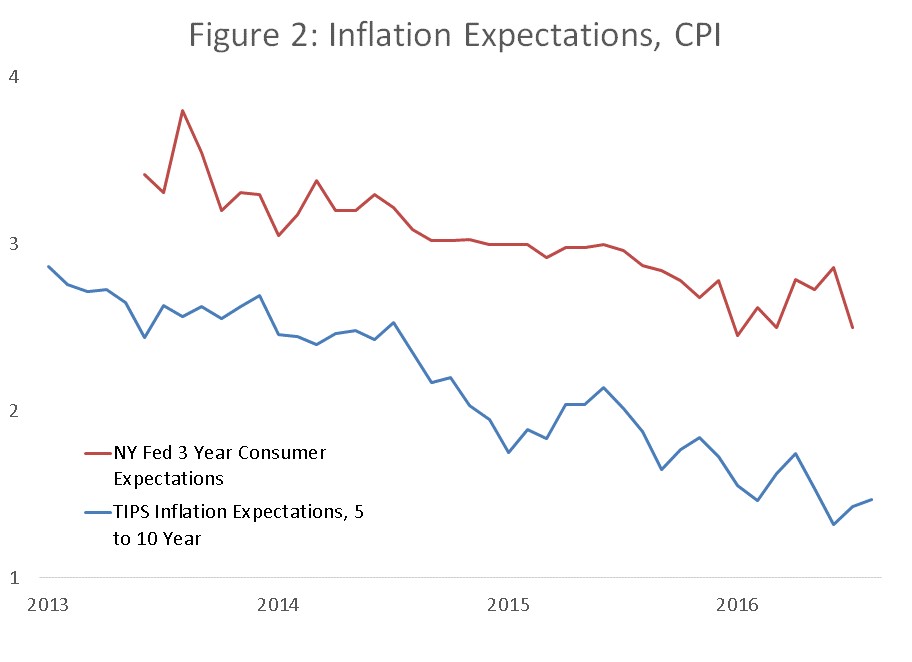

Even apart from the desirability of allowing inflation to rise above two percent in a happy economic scenario GDP, labor market and inflation expectations data all make a compelling case against a rate increase. Private sector GDP growth for the last year has averaged 1.3 percent a level that has since the 1960s always presaged recession. Total work hours have over the last 6 months grown at nearly their slowest rate since early 2010. And both market and survey measures of inflation expectations continue to decline.

My second reason for disappointment in Jackson Hole was that Chair Yellen, while very thoughtful and analytic, was too complacent to conclude that “even if average interest rates remain lower than in the past, I believe that monetary policy will, under most conditions, be able to respond effectively”. This statement may rank with Ben Bernanke’s unfortunate observation that subprime problems would be easily contained.

Rather I believe that countering the next recession is the major monetary policy challenge before the Fed. I have argued repeatedly that (i) it is more than 50 percent likely that we will have a recession in the next 3 years. (ii) countering recessions requires 400 or 500 basis points of monetary easing. (iii) we are very unlikely to have anything like that much room for easing when the next recession comes.

{kind=link}

Chair Yellen, relying heavily on research by David Reifschneider using the FRBUS model, comes to the relatively serene conclusion that by using forward guidance and QE policies—or LSAP (Large Scale Asset Purchases) in Fed parlance, the Fed will likely able to respond adequately to the next recession with its existing tool kit. I think this conclusion is unlikely to be right.

As Paul Krugman points out Reifschneider, working with John Williams and using the same FRBUS model, concluded that the ZLB was only a very small issue less than a decade before the financial crisis led to an 8 year stretch of zero rates. The market has been consistently wrong for most of the last decade on the ease with which interest rates could be raised by the Fed. And estimates of the neutral rate have been far lower for far longer than anyone would have predicted a decade ago. All of this suggests the need for substantial humility about what the Fed’s capacities will be the next time the economy encounters difficult times.

There is an important methodological point here—distrust conclusions reached primarily on the basis of model results. Models are estimated or parameterized on the basis of historical data. They can be expected to go wrong whenever the world changes in important ways. Alan Greenspan was importantly right when he ignored models and maintained easy policy in the mid 1990s because of other more anecdotal evidence that convinced him that productivity growth had accelerated. I believe a similar skeptical attitude towards model results is appropriate today in the face of the clear evidence that the neutral real rate has fallen. I pay attention to model results only when the essential conclusion can be justified with some calculation where I can see and follow each step.

Four more specific points deserve emphasis. First, Reifschneider assumes in is base case that the Fed funds rate reaches 3 percent before the next recession and treats as an extreme case the possibility that rates will reach only 2 percent before the next recession. As Jared Bernstein points out market expectations are much more pessimistic than this. According to the OIS market (basically long term fed fund futures) fed funds are expected even in the long run to rise only to 1.5 percent. This may be a bit misleading because the expected fed funds rate in 2020 of 1 percent includes some probability that it is zero because of a recession. Even so markets, which have been much more right than the Fed so far, are clearly signaling the likelihood that rates will be under 2 percent when the next recession comes.

I appreciate that Reifschneider takes seriously the possibility of secular stagnation by including a section on it. However, I fear he is overly sanguine in assuming that even under secular stagnation the Fed will start the next recession with an interest rate of 2 percent, as well as a ten year rate of 3 percent. This seems optimistic given both the market expectations discussed above and the fact that current interest rates are 0.50 percent nearly eight years after the last recession.

Second, though he downplays the significance, Reifschneider finds that the Fed will likely not have as much room to cut rates as it would like under the so-called “optimal control” method that Yellen has extolled in the past. Under this method the Fed is attempting to minimize the amount which inflation and unemployment differ from target over a series of years. In his simulations, the Fed is not able to use unconventional policies to fully achieve the equivalent of the nearly 12 percent rate cut it would otherwise desire. This shortfall is in response to a recession less severe than the recent one and with the questionable assumption that the Fed should view unemployment being too low as being as harmful as being too high.

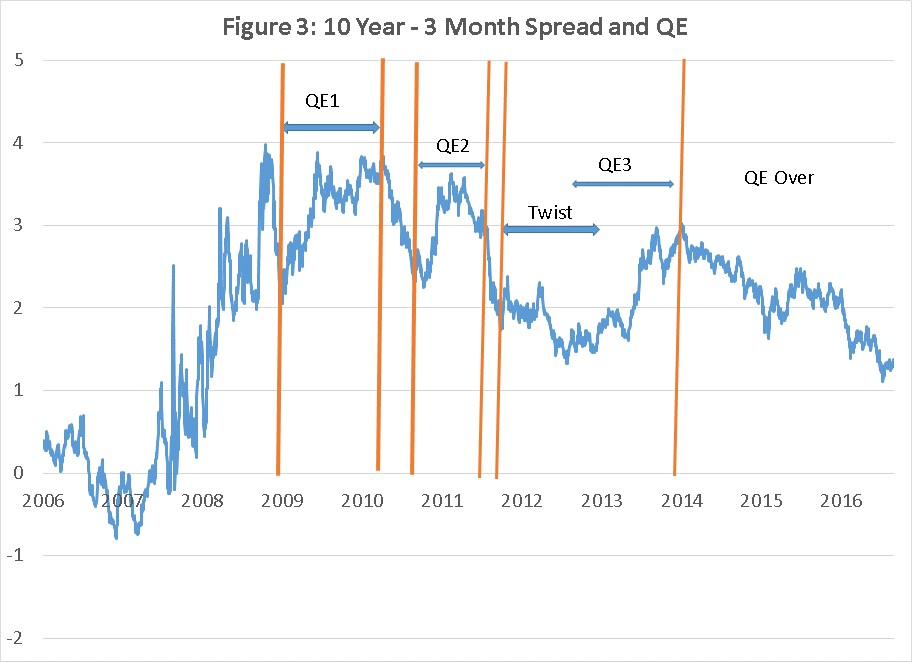

Third, I suspect that prevailing views at the Fed about the efficacy of QE and forward guidance substantially exaggerate their likely impact. I don’t think the Fed has taken on board the lesson of the three year period since QE ended. If longer term rates had risen after QE and forward guidance ended, this would surely have been taken as further evidence of their potency. It follows that the fact that term spreads have fallen substantially since the end of unconventional policy as shown in Figure 3 should lead to more skepticism about their efficacy.

On the issue of QE Greenwood, Hanson, Rudolph and I show that the contrary to much of the discussion during the QE period the stock of longer term public debt that the market has to absorb went up not down. The amount of longer term Federal debt that markets have to absorb is now as high as it has been in the last 50 years and long rates are extraordinarily low, as are term spreads. This calls into question the idea that price pressures caused by changing relative supplies are likely to have large impacts at times like the present when markets are functioning.

I wonder what credibility Fed forward guidance is likely to have given the utter disconnect over many years between Fed and market views regarding future rate and the track record so far of the Fed being wrong and the market being right.

Fourth, even if unconventional policy could be highly efficacious in moving long term rates and even if QE induced moves in long rates were potent, there is the question of how much room there is to bring down long rates. Reifschneider in his very careful paper shows that with a big recession rates would likely approach -6 percent, or even -9 percent, but for the zero lower bound. I find the idea that forward guidance and QE could do the anything like the work of 600, let alone 900, basis points of rate cutting close to absurd. Both QE and forward guidance are said to work by bringing down longer term rates. The 10 year Treasury is now in the 1.6 percent range. If the Fed returned Fed Funds to its lower bound level in the context of a recession, I would expect to see 10 year rates fall substantially perhaps to 1 percent without any QE or forward guidance. How much room is there for unconventional policy to bring them down further? Reifschneider ‘s assumption that there will be room for unconventional policy to bring down 10 year rates by hundreds of basis points seems to me very doubtful.

To put the point differently, typically in recessions the 10 year Treasury has declined from peak to trough by around 1.8 percentage points. Even if the rate got to European or Japanese levels, surely an unappealing prospect, there may not be enough room to bring down long rates to assure prompt recovery.

On balance, I think the Fed’s complacency about its current toolbox is unwarranted. If I am wrong in either exaggerating the risks of recession or understating the efficacy of policy, the costs of taking out insurance against a recession that cannot be met with monetary policy are relatively low. If I my fears are justified, the costs of complacency could be very high. The right policy in the near term should be tilting as hard as possible against recession as argued in the first blog in this series. For the longer term the Fed will have to reconsider its broad policy approach. This will be subject of my next entry.