As the Fed meets today and tomorrow, I am increasingly convinced that while they have been making reasonable tactical judgements their current strategy is ill adapted to the realities of the moment. Exuding soundness is the task of policymakers. Provoking thought is the task of academics. So here are some not entirely formed reflections.

Japan’s essential macroeconomic problem is no longer lack out output growth. Unemployment is low. Relative to its shrinking labor force, output growth is adequate by contemporary standards. Japan’s problem is that it seems incapable of achieving a 2 percent inflation. This makes it much harder to deal with debt problems and leaves the Japanese with little spare powder if a recession comes.

I am reluctantly coming to the conclusion that the United States may be on a slow-motion trajectory towards a Japanese chronic lowflationary or even deflationary outcome. A corollary of this view is that the current hawkish inclination of the Fed, with its chronic hope and belief that conditions will soon permit interest rate increases, is misguided. The greater danger is of too little rather than too much demand. A new Fed paradigm is therefore in order.

Any consideration of macro policy has to begin with the fact that the economy is now seven years into recovery and the next recession is on at least the far horizon. While recession certainly does not appear imminent, the annual probability of recession for an economy that is not in the early stage of recovery is at least 20 percent. The fact that underlying growth is now only 2 percent, that the rest of the world has serious problems, and that the U.S. has an unusual degree of political uncertainty all tilt toward greater pessimism. With at least some perceived possibility that a demagogue will be elected as President or that policy will lurch left I would guess that from here the annual probability of recession is 25-30 percent.

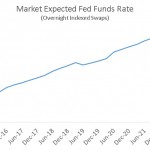

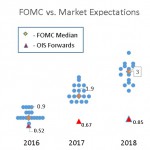

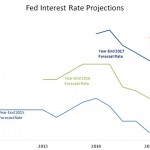

This seems to me the only way to interpret the yield curve. Markets anticipate only about 65 basis point of increase in short rates over the next 3 years. Whereas the Fed dots suggest that rates will normalize at 3.3 points, the market thinks that even 5 years from now they will be about 1.25 percent.

Markets are thinking that recession will come at some point and when it does rates will go to near zero. As a rough calculation, if it is assumed rates will be raised twice a year with continued growth than the 85 basis point estimate for fed funds in December 2018 implies a 50 percent chance of recession by then.

So both history and markets are telling us that we are in the shadow of possible recession.

What does this mean? First it implies that if the Fed is serious — as it should be – about having a symmetric 2 percent inflation target then its near term target should be in excess of 2 percent. Prior to the next recession — which will presumably be deflationary — the Fed should want inflation to be above its long term target.

The point can be put in one more way. The Fed’s dots forecast refer to a modal scenario of continued recovery. They see inflation rising to 2 percent only in 2018. Why shouldn’t they prefer a path with more demand, inflation at target sooner, more stimulus as recession insurance, and a small margin of extra inflation as a buffer against the next recession? Those who think that raising rates somehow helps prepare to be counter-cyclical are confused. Given lags raising rates now would increase the chances of recession along with the likely severity. Raising inflation and inflation expectations best prevents and alleviates recession.

There is the further point that the logic that led to the adoption of the 2 percent inflation target years ago suggests that it is too low now. As brought out in a famous colloquy between Janet Yellen and Alan Greenspan[1] the case for a positive inflation target balances the benefits of stable money with the output cost of lowering inflation and two ways that positive inflation is helpful—the periodic need to have negative real rates, and inflation’s role in facilitating downward adjustment in real wages given nominal rigidities.

All of the factors pointing towards a higher inflation target have gained force in recent years. Regardless of whether they believe in secular stagnation, almost everyone agrees that neutral real rates have declined 100 basis points or more. This means there will be more frequent need for negative real rates. Slowing underlying wage growth means that there is more pressure for downward adjustments that are facilitated by inflation. Experience has proven that Yellen was correct to be skeptical of the idea very low inflation rates would improve productivity. And it is plausible that the error in price indices has increased with the introduction of new categories of innovative and often free products.

This means that if a two percent inflation target reflected a proper balance when it first came into vogue decades ago, a higher target is probably appropriate today. This is another reason to allow inflation to rise above 2 percent.

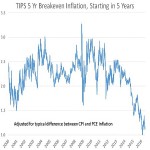

Second, the theoretical consideration that the Fed should not raise rates until inflation is clearly above target is reinforced by the current data flow. Long term inflation expectations are depressed and declining, as shown in TIPS (inflation-indexed) government bonds, which I have adjusted to the Fed’s preferred PCE price index. Note that expected inflation is back near record low levels despite oil prices having risen about 70 percent from their February levels.

The Fed has in the past counterbalanced declines in market inflation expectation measures by pointing to the relative stability in surveys-based measures. This argument is much harder to make now that consumer expectations of inflation have broken decisively below their all-time lows even as gas prices have been rising.

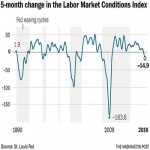

There is of course the question of a possibly overheating labor market as a source of future inflation. While last month’s highly disappointing employment report was a jolt to most observers, the Fed’s summary employment conditions index has been flashing yellow since the beginning of the year. Declines in this measure have presaged recession half of the time and uniformly been followed by rate reductions rather than rate increases.

Embedded inflation expectations are low and declining. Comprehensive measures of the labor market are deteriorating and growth is at best mediocre. Meanwhile inflation is clearly below where the Fed should want it. The right concern for the Fed now should be to signal its commitment to accelerating growth and avoiding a return to recession, even at some cost in terms of other risks.

This is not the Fed’s policy posture. Watching the Fed over the last year there is a Groundhog Day aspect. One senses they really want to raise rates and achieve a more “normal” stance. But at the same time they do not want to tighten when the economy may be slowing or create financial turmoil. So they keep holding out the prospect of future rate increases and then find themselves unable to deliver. But they always revert to holding out the prospect of rate increases soon, partly for internal comity and partly to preserve optionality.

Over the last 12 months nominal GDP has risen at a rate of only 3.3 percent. We hardly seem in danger of demand running away. Today we learned that Germany has followed Japan into negative 10 year rates. We are only one recession away from joining the club. The Fed should be clear now that its priority is not preventing a small step up in inflation, which in fact should be welcomed, or returning interest rates to what would have been normal to a world gone by. Instead the Fed should focus on assuring adequate growth in both real and nominal incomes going forward.

_______________________

[1] https://www.federalreserve.gov/monetarypolicy/files/FOMC19960703meeting.pdf pp.42-50. Yellen: “As I total things up, it appears to me that a reduction of inflation from 3 percent, which I take as roughly our current level, to 2 percent, very likely, but not surely, yields net benefits. The “grease-the-wheel” argument is of minor importance at that point, and tax effects could be significant. But with further reductions in inflation below 2 percent, nominal rigidity begins to bite so that the marginal payoff declines and then turns negative. To my mind, to go below 2 percent measured inflation as currently calculated requires highly optimistic assumption about tax benefits and sacrifice ratios.”