I had high hopes for the Federal Reserve’s annual Jackson Hole conference. The conference was billed as a forum that would look at new approaches to the conduct of monetary policy—something that I have been urging as necessary given secular stagnation risks and the sharp decline in the apparent neutral rate of interest. And Chair Yellen’s speech in a relatively academic setting provided an opportunity to signal that the Fed recognized that new realities required new approaches.

The Federal Reserve system and its Chair are to be applauded for welcoming challengers and critics into their midst. The willingness of many senior officials to meet with the Fed Up group is also encouraging. And its important for critics like me to remember that the policy explorations of today often become the conventional wisdom of tomorrow. In this regard the fact that the Fed has now recognized that the decline in the neutral rate is something that is much more than a temporary reflection of the financial crisis is a very positive sign.

On balance though, I am disappointed by what came out of Jackson Hole judging by press reports since I was not there. First, the near term policy signals were on the tightening side which I think will end up hurting both the Fed’s credibility and the economy. Second, the longer term discussion revealed what I regard as dangerous complacency about the efficacy of the existing tool box. Third, there was failure to seriously consider major changes in the current monetary policy framework.

I shall argue each of these points in a blog series this week. At the outset however, it is important to recognize that the Fed has not earned the right to be intellectually complacent or to expect that others will have faith in its current policy framework. Given the Great Recession and its forecasting record, it is not surprising that Gallup has found that public confidence in the Fed has sharply declined in recent years, though it has increased recently.

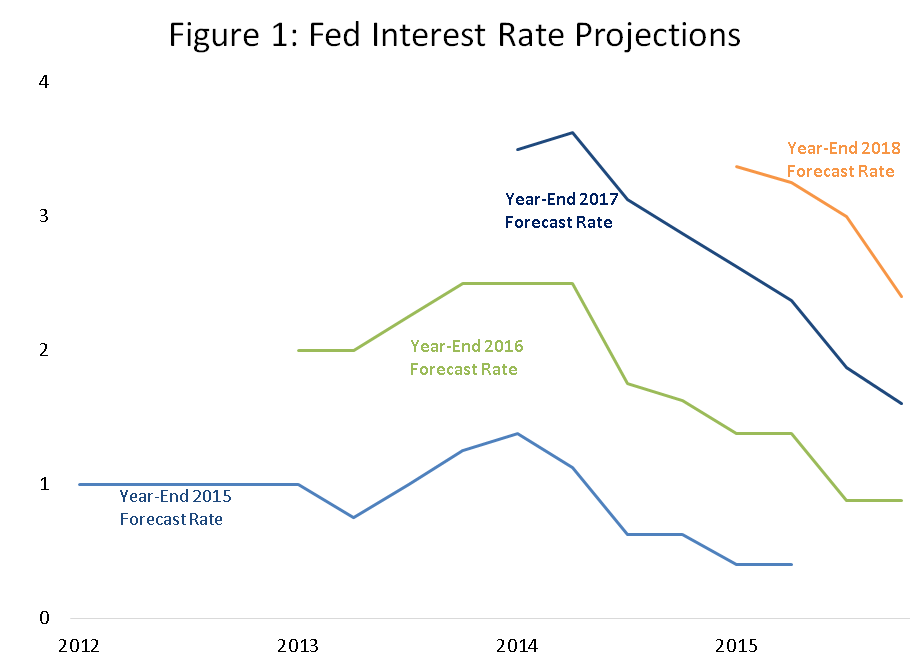

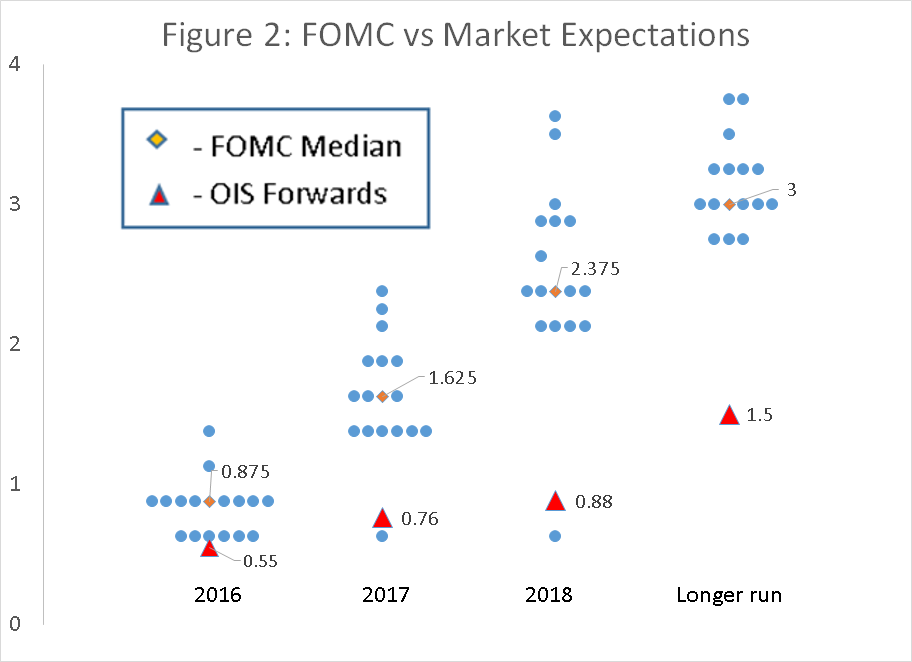

For nearly a decade, since the mid 2008 FOMC meetings where many believed that the worst had past, the Fed been too serene about the economic outlook and a return to past regularities. When the Fed predicted last December that it would raise rates four times in 2016, market participants saw a disconnect from reality. It has been that way for a long time. Figure 1 shows the Fed’s forecasts of its future monetary policies since they began releasing them. The Fed has always believed that rate increases and normalization were around the corner but never been able to deliver. Figure 2 looks at the current situation showing the “dots” reflecting Fed forecasts and the market’s prediction of future interest rates. The divergence between the market and even the dovish end of Fed forecasts is clear.

Near Term Policy

Chair Yellen in Jackson Hole basically repeated the existing Fed position that rates would be raised at some point when the data were clear that the economy was strong and inflation reaching two percent. Markets took the remarks as mildly dovish until Vice Chair Fischer was seen on CNBC as interpreting the Chair as implying that two rates increases by the end of the year were possible at which point interest rates across the spectrum rose fairly sharply and stock prices fell.

The right signal to have sent in my view was very dovish. The Fed has emphasized that its two percent inflation target is a symmetric one. Its current forecast is for a strong economy that will next Spring enter its 9th year of recovery. If inflation should not be allowed to rise a bit above two percent in such circumstances, how can it be expected to average two percent over time given that recessions and downturns at some point are inevitable? I hoped that the Fed would make clear that it would tighten only when there appeared a real risk of inflation expectations rising above two percent. At a time when market forecasts of inflation on Fed’s preferred price index are in the range of 1.2 percent, this is very likely some time off. Some are skeptical of market measures of inflation expectations. Note that survey measures of long term inflation expectations for both professionals and consumers are near historical lows and if anything have declined over the last year.

{kind=link}

Additional points that I would have thought appropriate in commenting on near term policy include: (i) With current estimates of the real neutral rate running near zero and there being a downward trend it is far from clear that current policy is highly expansionary. (ii) It is plausible that hysteresis effects account for some of the decline in productivity growth and that if so allowing for rapid demand growth might have lasting supply side benefits. (iii) If a two percent inflation target was appropriate when the neutral real rate was thought to be two percent and stable, surely a higher target is appropriate when the neutral real rate is zero and unstable. (iv) In contrast to the risks of inflation exceeding two percent ,which are likely very small, the risks of a downturn are very serious. (v) The apparent rigidity of inflation expectations and insensitivity of inflation to measures of slack create extra uncertainties about the conventional idea that unemployment rates in the 4.5 percent range risk accelerating inflation.

I agree with Chair Yellen’s observation that the case for a rate increase now is stronger than it was a few months ago. The economy certainly does appear to be gaining strength in the second half of the year, the Brexit shock has been easily absorbed, and markets are unusually calm. But to say that the case for a rate increase has strengthened is not to say that it has reached the point of being persuasive.

Even if the September employment report is strong, I do not see a case for a September rate increase. There is no imminent danger of repeating the 1970s experience where inflation expectations ratcheted up leading to stagflation. If a greater than 1/3 chance of a rate increase in September was not in markets, the cost of credit for small business would be lower and mortgage rates would decline. Employers would be more confident about hiring. And pressures would be removed from emerging markets. The world economy would be more robust.